Tax Advice

How to Enjoy a Stress-Free U.K. Tax Season With FreshBooks

Even though it comes every year, getting your business ready for tax season can be daunting and stressful. There’s nothing more annoying than realising you’ve forgotten a major expense just as you’re about to file your return. (Who hasn’t been there?) And with new rules like Making Tax Digital (MTD) in the mix, it can seem like there are only more complications to wrap your head around.

But cloud accounting software like FreshBooks can make filing your taxes much easier. FreshBooks is MTD-compatible and HM Revenue & Customs (HMRC)-approved. Plus, tools like expense tracking and accounting reports keep you on top of your business all year round.

Here are 6 ways FreshBooks helps you manage your books.

![]()

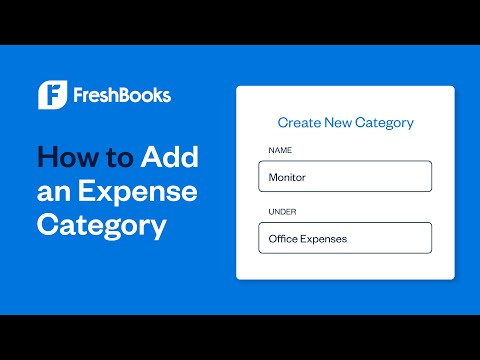

1. Automatic Expense Tracking

There’s nothing fun about scrambling through receipts just before your return is due. With FreshBooks, you can automatically track your expenses all year round. This helps you know what you’re spending each month and lets you stay on top of your cash flow.

Start by connecting your bank account and credit cards to FreshBooks and automatically import expenses into your FreshBooks account. Not only will you know exactly what you’re spending and when, but you’ll save countless hours manually entering numbers. That’s time you can better spend on pleasing your clients.

Once you’ve imported your expenses, it’s time to categorise them to track your spending in FreshBooks. By setting up expense categories in FreshBooks, moving forward, you can quickly sort and classify expenses as you spend money. Then, come tax season, it’s a piece of cake to assess your books for allowable expenses and thus reduce your taxable profit.

Another useful tool for managing your expenses in FreshBooks is the Bulk Actions button. This feature allows you to change the merchant, category, or VAT for up to 50 expenses or assign multiple expenses to a Client or Project with the click of a button.

2. Double-Entry Accounting

Have big plans to grow your business? Then it’s important to understand double-entry accounting, the industry-standard method that bookkeepers and accountants use to track and manage business financial records.

Double-entry accounting means you need to create 2 entries for each business transaction: a debit and a credit. For example, imagine you just bought a new laptop for your business. The double-entry system tracks the purchase as a credit for the cost and a debit for your new asset. This helps you keep accurate records of your profits and losses. Which, in turn, enables you to lower the chances of making errors on your tax return.

It might sound complicated at first, but FreshBooks designed a double-entry accounting system that’s simple and easy to use. With Plus or Premium plans, you get access to 8 essential functions:

- Cost of Goods Sold. Associate your expenses with the costs of delivering goods and services to your clients.

- Other Income. Track income outside of your invoices so you can view all your earnings in one place in your Profit and Loss Report (P&L).

- General Ledger. See the full history of all your business’s financial transactions. This is useful for completing your payment on account.

- Trial Balance. View the debit and credit balances in your chart of accounts.

- Chart of Accounts. Refer to a list of all the accounts for categorising your business transactions.

- Accountant Access. Let your accountant see all your financial information and access double-entry accounting features with their own log-in.

- Bank Reconciliation. See anything that doesn’t add up and fix errors in real time.

- Balance Sheet. Get a complete record of your business’s assets, equity, and liability at any point in time.

When you use FreshBooks’ double-entry accounting functions, you open up a new world of business insights, opportunities to collaborate with accounting professionals, and unbeatable precision during tax season.

3. Bank Reconciliation

Bank reconciliation allows you to compare your cash account with your bank statement and check for mismatches. This process can be tricky at best, and issues usually arise because of timing.

Why bank reconciliation is important (3 examples):

- You write a cheque at the end of the month and record it immediately, but your bank records this the next month

- A client makes a payment into your account at the end of the month, and the bank immediately records it, and you only become aware of it the next month

- The bank debits your account for bank charges or even interest on your overdraft in one month, and you only see those deductions when you receive your bank statement

When you’re on top of bank reconciliation, you’ll spot these discrepancies, and you’re less likely to spread errors to your other financial statements. Fewer errors mean less stress at tax time.

FreshBooks automatically imports and organises your cash transactions. You can approve matching suggestions against your bank statement; mark transactions as transfers (between accounts), owner’s equity, or expense refunds; and view monthly reconciliation reports to see if anything else needs to be paired together.

With fewer bank reconciliation errors, you’ll spend less time sorting through past financial records, leaving more time for actual client work.

4. Accountant Access

If you already work with an accountant, you know how valuable they are. From offering financial advice to balancing your books in time for tax season, their services are a worthy investment in your business.

But working with your accountant can get tricky when you aren’t on the same platform. Numbers can be lost in translation, and emailing reports back and forth isn’t ideal.

That’s why it’s so important to use accounting software you can both access, like FreshBooks. By inviting your accountant to join with their own personalised log-in, they’ll see your financial reports and double-entry accounting tools. They’ll have a complete picture of your books all year round. This is useful for submitting your tax return, and it’ll help them offer you advice at any time.

In FreshBooks, your accountant can:

- Access your General Ledger, Balance Sheet, and Profit and Loss reports

- Add Journal Entries

- Manage your Chart of Accounts

- Review your Invoices, Expenses, Payments, Other Income, and Bank Reconciliation

5. MTD Compatibility

If you’re VAT-registered and earn above £85,000, HMRC requires you to keep digital records of your taxable income. You’ll need to send VAT returns using MTD-compatible software too.

Self Assessment taxpayers, which includes self-employed business owners and landlords earning above £50,000, must adhere to MTD rules by April 2026.

FreshBooks is MTD-compatible. You can easily create VAT return reports for your accountant to review before filing them directly with HMRC from your FreshBooks account. Say goodbye to late filings and hello to submitting on time every time.

6. Quarterly VAT Returns

Many businesses need to send quarterly VAT returns to HMRC. These are due 1 month and 7 days after the end of each accounting period. Late filing, inaccuracies, and late payments can all lead to financial penalties. You can also be penalized for filing a paper return beyond the MTD compliance date.

FreshBooks helps you to avoid penalties like this. When all your transactions are recorded in real-time, you won’t have to estimate what you owe each quarter. You’ll already have a clear picture of where your business stands and what you owe.

A Hassle-Free Tax Season

Tax time doesn’t have to be daunting or stressful. While tracking your expenses and getting to know new rules like MTD can be scary, using MTD-compatible and HMRC-approved software like FreshBooks makes staying on top of your business finances so much easier throughout the year.

Give Barclaycard Payments a Try Too! (VIDEO)

Start a Free 30-Day Trial Today

Ready to try FreshBooks to stay on top of your books all year round? Sign up for a free 30-day trial.

This post was updated in January 2024.