When you’re the boss, getting your first paycheck can be a very meta experience.

Figuring out how to pay for yourself as a business owner can be complicated – but we promise, it’s not as crazy as it seems.

That pay stub reflects all the hard work it took to bring your successful business to life. And when you get to enjoy that moment, it can be a fantastic thing to experience.

In this post, I’ll show you exactly how to pay yourself—you, the boss, the business owner, the one in charge, the one taking risks.

![]() Table of Contents

Table of Contents

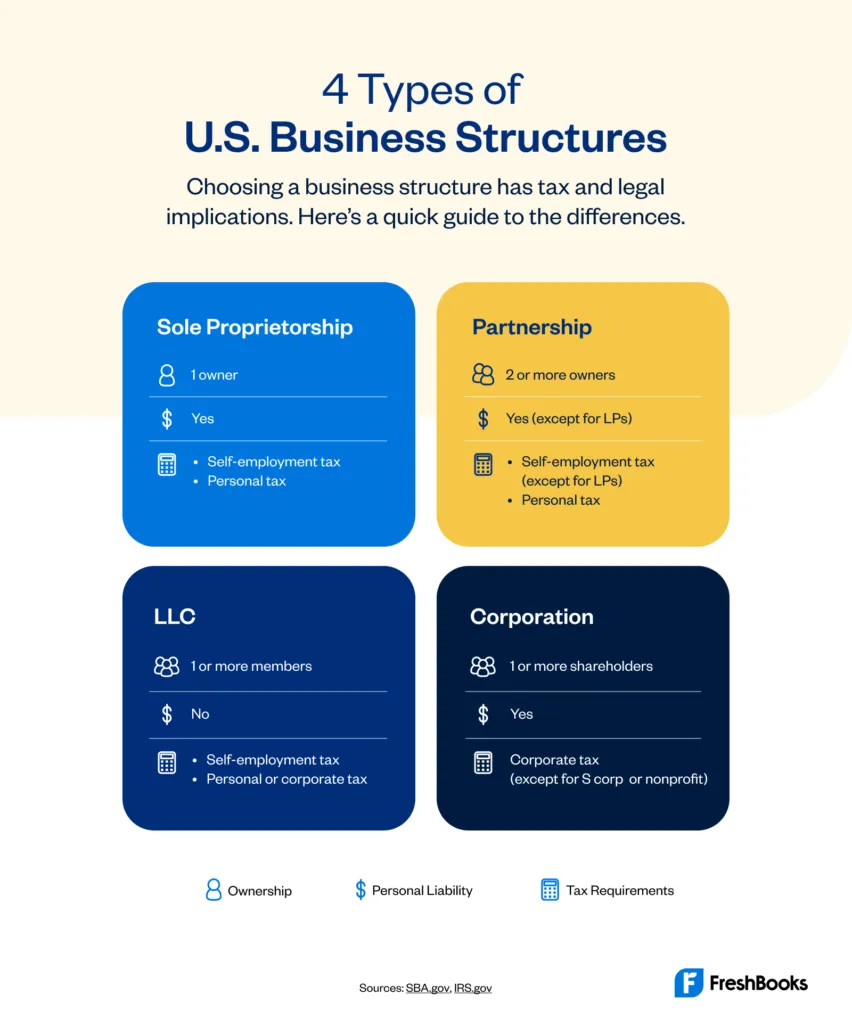

1. Determine Your Business Structure

Your business structure is where it all begins. In fact, it’s the foundation for the entire payroll process and will help point you to the payment style that’s right for you.

You’ve likely heard terms like Sole Proprietorship or Sole Proprietor, Partnership, Limited Liability Company (LLC), Corporation, and Cooperative.

Oh, you already know your entity? Bravo, scroll down to the next step.

If not, this business structure overview (it also discusses how you pay taxes) can give you a good idea of what options are out there. Before finalizing your decision, remember to schedule some time with your accountant to help explain the ins and outs of each specific business structure, the tax implications, and which is right for you.

2. Figure Out the Best Payment Method

How to Decide What U.S. Business Structure Is Right for You

How to Decide What U.S. Business Structure Is Right for You How Your Business Structure Affects Your U.S. Taxes

How Your Business Structure Affects Your U.S. Taxes How to Set Up Payroll: Everything U.S. Small Business Owners Need to Know

How to Set Up Payroll: Everything U.S. Small Business Owners Need to KnowNow, think about how you’d actually like to pay yourself.

This part depends on a few factors like your entity type, business plan, and years in operation. Here are two main types of payments you should know about.

A. Draw

Most small business owners pay themselves through something called an owner’s draw. The IRS views owners of a Limited Liability Company (LLC), a sole proprietorship, and a partnership as self-employed. As a result, the small business owner isn’t paid regular wages. That’s where the owner’s draw comes in.

It’s important to note that draws aren’t taxed at the time they’re taken out. Instead, the IRS taxes owners of these types of businesses on all business profits, whether you take it out as a draw or leave it in the company.

Which business entity are draws suited for? Sole proprietorship, LLCs, or partnerships. If you’re an S corporation (also called S corp), you’ll also have the option to take an owner’s draw in addition to your regular salary.

B. Salary

Salaries are set, recurring payments that the state and federal governments tax. Suppose you own a corporation and are involved in the day-to-day operations. In that case, the IRS will expect you to take a “reasonable” salary (more on what constitutes reasonable compensation later).

Which business entity is salary suited for? C corp and S corp.

Here’s a quick breakdown of what a C corporation and S corporation are.

C Corporation: A C corporation, or C corp, is a legal entity separate from its owners. Corporations can profit, be taxed, and be held legally liable.

Corporations offer the most substantial protection to their owners from personal liability. Still, the cost to form a corporation is high and requires more extensive record-keeping, operational processes, and reporting.

Unlike sole proprietors, partnerships, and LLCs, corporations pay income tax on their profits. In some cases, corporate profits are taxed twice—once as business profits, then again when those profits are paid out to shareholders in the form of dividends.

Corporations have an advantage when it comes to raising capital because they can raise funds by selling stock, which can also benefit attracting employees.

S Corporation: An S corporation, or S corp, is designed to avoid the double taxation drawback of regular C corps. S corps allow profits, and some losses, to be passed through directly to the business owners’ personal income tax return without ever being subject to corporate tax rates.

Not all states tax S corps equally, but most recognize them the same way the federal government does and tax the shareholders accordingly. Pro tip: Whatever payment style you choose, keep in mind that you will eventually have to pay taxes on that amount, if not immediately, then at some point down the road.

Planning for this ahead of time is crucial, so you’re not stuck with a giant tax bill when you least expect it. Payroll solutions such as FreshBooks Payroll, powered by Gusto, will automatically handle this for you, so do your research upfront.

3. Select an Amount

Okay, now we’re getting to the good part—how to pay yourself as a business owner.

Once you’ve determined the right type, your next job is to calculate how much to give yourself. Wait, I’m the business owner. Can’t I just pick any number? Well, not exactly. You want to pay yourself an amount that ties to your duties and sets your business up for long-term success.

Spend some quality time with your profit & loss (P&L) statements to see how much net profit you’re raking in each month. Then, deduct your own pay from that amount—not the total revenue. This is because you want to pay yourself from the amount left over (in your small business bank account). This happens after you tackle your important business expenses, like supplies, rent, paying your team, and everything else needed to keep your venture running smoothly.

The IRS also requires that all employer compensation is considered reasonable compensation (according to Publication 535), which just means that it should match the amount you’d make if you were working in the same role at another company.

If you feel like you wear a million different hats, try to pick out the most common responsibilities you take on aside from just being the business owner, and then determine how much you would have to pay someone if you outsourced those tasks. This is sometimes referred to as your “true wage,” and it’s truly cool to think about your job and your own business in such a multifaceted way.

4. Pick a Payroll Schedule

If your business has at least one employee (including yourself!), you need to think about how often you want to pay yourself. In the U.S., the most popular payroll schedules are twice a month, every two weeks, and weekly.

Most states require that you follow a basic calendar, so find where your state falls on this chart from the Department of Labor. The basic rule is that you can always pay yourself more often but never less than your state’s particular schedule.

A perfect cadence to consider is the 15th and last day of each month, as not every month has the same number of days, but this is a way to create a predictable schedule.

FreshBooks Payroll, powered by Gusto, is a full-service, embedded payroll solution that links all your payroll and finances in one easy-to-use place–giving you the complete picture of your business.

5. Get Your Paycheck

Okay, small business owners, you’re speeding toward the finish line: Now it’s time to actually get paid. This is a huge milestone for your business, so use it as a moment to celebrate all you’ve accomplished as a small business owner.

Getting paid can be as easy as writing a check and depositing it into your personal bank account, or even quicker if you go the direct deposit route. Direct deposit simply means that the money is taken from your business bank account and dropped straight into your personal bank account.

Before picking between the two, make sure you know exactly when you’ll have access to the amount so you can properly plan ahead.

Are You Prepared to Pay Yourself?

Paying yourself for the first time as small business owners isn’t just about earning money—it’s about earning money from the very idea you believe in. And when that day finally swings around, you can sit back, relax, and gloriously watch as all your sweat and sacrifices pay off.

From business plan to business growth and beyond, a lot of small businesses don’t make it this far so kudos to you and your growing team.

What was the most exciting thing you felt the first time you got to pay yourself as a small business owner? I’d love to hear about your experience in the comments below.

This post was updated in December 2024.

Written by Tomer London, Co-Founder and Chief Product Officer, Gusto

Posted on August 27, 2021

This article was verified by Janet Berry-Johnson, CPA and Freelance Contributor

Freshly picked for you

FreshBooks for Accountants: 7 New and Updated Features for 2025

FreshBooks for Accountants: 7 New and Updated Features for 2025

What Canada’s GST/HST Holiday Tax Break Means for Small Businesses

What Canada’s GST/HST Holiday Tax Break Means for Small Businesses

Now You Can Pay Your Entire Team, Including Contractors, Using FreshBooks Payroll

Now You Can Pay Your Entire Team, Including Contractors, Using FreshBooks Payroll

How Mackenzie and Natasha Bring Order to Chaos With FreshBooks, One Client at a Time

How Mackenzie and Natasha Bring Order to Chaos With FreshBooks, One Client at a Time

Accounting Professionals: Here’s What to Look for in General Ledger Software

Accounting Professionals: Here’s What to Look for in General Ledger Software

Free guide: The Business Owner’s Guide to Collaborative Accounting™

Free guide: The Business Owner’s Guide to Collaborative Accounting™