Scaling Your Business

Stressed About the Future of Your Business? You Need Cash Flow Forecasting

Do you ever wonder about the optimal time to hire a team member, rent an office space, or invest in a new piece of equipment? You want to make sure you have enough money coming in to support the investment and not too much money flowing out.

Most business owners wrestle with cash flow questions like this, especially when they’re in growth mode. What’s the answer? Cash flow forecasting. Understanding where you stand financially—not just in the present, but in the future as well—will help you confidently make sound business decisions.

![]()

What Is Cash Flow Forecasting?

A cash flow forecast shines a light on how much cash your business is projected to have over a specific period of time, using current and historical income/expenses data.

This cash flow data can help you:

- Identify the right time to make capital investments

- Understand the impact of regular expenses on your cash flow

- Consider how to optimize your invoicing and accounts receivable processes

- Assess when your business is busiest and slowest

You can do forecasts for the short-term (30 days), medium-term (2 months–1 year), or long-term (1–5 years). It’s important to note that a longer forecasting period results in a less accurate forecast. (Unless you have access to a crystal ball.)

Cash Flow Forecast vs. Cash Flow Statement

The difference between your statement and forecast is simple: A cash flow statement (or report) shows actual data on past cash flows in and out of your business. A cash flow forecast (or projection) is an estimate based on the information you’ve gathered in your statements/reports.

That means you’ll need accurate cash flow reporting in place first to do accurate cash flow forecasting.

Why Do I Need to Do a Cash Flow Forecast?

Managing a business can sometimes feel like a day-by-day proposition, but most businesses can’t achieve strong, sustainable growth unless they establish working capital. And you can’t make informed decisions or plan ahead to meet business objectives without a strong grasp of your financials.

Let’s say you want to bring on an administrative assistant to help lighten your load so you can focus more on client work. You might look at how much money you have in the bank right now and think you could pay an employee’s salary this month, no problem.

But can you predict your cash levels next month? Or in 3 or 6 months? The question becomes, will your company have the cash to support the ongoing expense of hiring an employee? This is where a cash flow forecast comes in.

Understanding the big picture of your cash flow, including what comes in (and when) and what goes out (and when) will allow you to discern what’s feasible for your business now, and in the future.

How Do I Calculate My Cash Flow?

The key is to nail down all the cash coming in and going out. Here are some examples:

Cash Inflows

- Paid invoices

- Bank loans

- Government grants

- Income from a rental property

- Sale of assets (e.g., equipment)

Cash Outflows

- Regular payments (e.g., rent, utilities, travel, software subscription, business mobile phone)

- Loan payments

- Equipment purchases

- Employee salaries

- Tax payments

The best way to get accurate info? Dig into your accounting solution’s financial reports. The numbers are all there.

Cash Flow Reports You Need

The two most important reports for forecasting cash flow (both available to FreshBooks customers) are the Profit & Loss Report and the Cash Flow Report. Both of these are key to pinpointing the pattern of your earning and spending, and creating a cash flow statement you can use in your decision-making process.

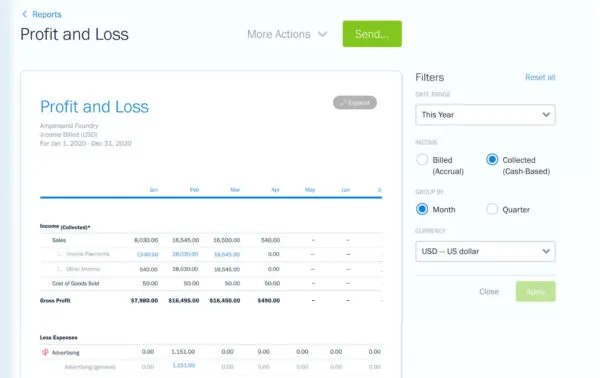

Profit-and-Loss Report (a.ka. P&L, Profit-and-Loss Statement, Income Statement)

Most accountants will tell you that the profit-and-loss report is the mother of all reports when calculating and forecasting your business’s cash flow.

If you enter all of your paid invoices and expenses into your cloud accounting software, you can see your P&L figures with the click of a button. What it shows is:

Gross Profit – Expenses = Total Net Profit

Gross Profit: Your net income (all sales entered, including billed and paid invoices and other income, less credit notes and adjustments) minus cost of goods sold (COGS).

Expenses: All expenses entered, including bill payments and other outgoing money

By subtracting your total expenses from your gross profit, the net profit shows exactly how much you earned (or lost) after expenses.

You can set your P&L report to measure a given period—such as a month, a quarter, or even a whole year—to show your earning and spending patterns. This is the key factor in cash-flow forecasting.

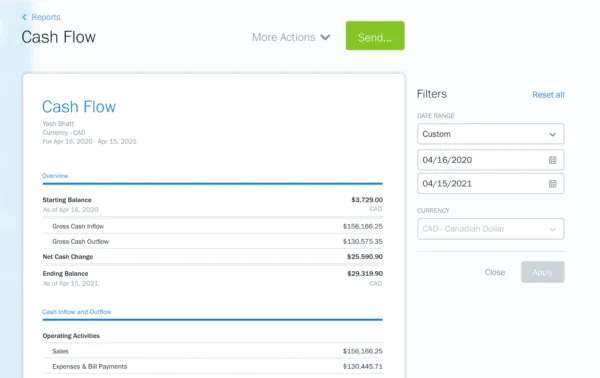

Cash Flow Report (a.k.a. Cash Flow Statement)

Want a quick snapshot of how much cash you have on hand, and what’s been entering and leaving your business? A cash flow report is an important tool that breaks it down for you.

The cash flow report has several sections:

Starting Balance: Your total cash balance at the start of the reporting period.

It is the sum of: Gross Cash Inflow (the total of all money-in transactions that impact any cash accounts) + Gross Cash Outflow (the total of all money-out transactions that impact any cash accounts)

Net Cash Change = Gross Cash Inflow – Gross Cash Outflow

Ending Balance = Starting Balance + Net Cash Change

The Ending Balance is your net cash flow over the period of time you’ve selected for your report.

Now that you know the calculations you need to see where you stand, you can look for patterns that will help project cash flow and improve your future cash flow.

How Do I Forecast My Cash Flow?

If you take a deep dive into your P&L over the last several months or last. year, you’ll no doubt walk away with some insights about how you’re earning and how you’re spending.

Be realistic about what you can expect from your business. The exercise is also an opportunity to correct some inconsistent or troubling patterns. For example, if you’ve seen a negative cash flow in Q3 for the last 3 years, you can also expect a similar cash position in the third quarter this year, unless you make some changes.

At the same time, you can also manipulate the future by detecting earning/spending patterns and setting out to correct any imbalances.

Here’s an example of a forecasting process you might use:

Cash Flow Forecasting in 4 Steps

Step 1: Choose a forecasting period, e.g., the next calendar or business year.

Step 2: Review your sources of cash over the previous year (or 2 years, if you think that will give you a more accurate picture). For the forecasting period, ask yourself:

- Will I still work with the same clients regularly? Can I expect to work with them for the foreseeable future?

- Will I take out any loans, sell assets, or receive investment income or government grants?

- Have I or will I be signing a long-term contract with a large client that will extend into the forecast period?

Using your cash inflows from the previous year(s), consider how the above factors could increase or decrease cash receipts next year, and estimate.

Step 3: Review cash outflows over the previous year (or 2 years). For the forecasting period, ask yourself:

- Will my regular expenses (utilities, rent, loan payments, etc.) be the same?

- Will I buy any assets or pay back any loans?

- Will I have any other one-time expenses?

Using your operating costs from the previous year(s) and the things that may be different in the near future, estimate your cash outflows for the next year.

Step 4: Revisit your cash flow report to determine your current cash on hand. Add the cash inflows and deduct the outflows for the coming year. This will be the closing cash balance for the conclusion of the next year—and the opening cash balance for the year after.

An Accurate Cash Flow Forecast Can Supercharge Your Business

The time you invest in being a detective in your business’ financials will help you make smart decisions for the future. You’ll know what to expect and how you can alter that expectation by tweaking behaviors based on the insights of your inquiry.

As with any forecast or projection, things can go awry. (Hello, global pandemic.) Or, you could even run into problems when things go great. It’s not unusual for rapid growth to disrupt cash flow for small businesses. (Read how to solve the most common cash flow problems.)

But, with a well-documented cash flow forecast in hand, the next time you’re wondering whether you should spring for a new office space or a shiny new piece of equipment, you can confidently circle a date on the calendar.