Tax Advice

Bookkeeping vs. Accounting: What’s the Difference—and Which One Does Your Business Need?

![]()

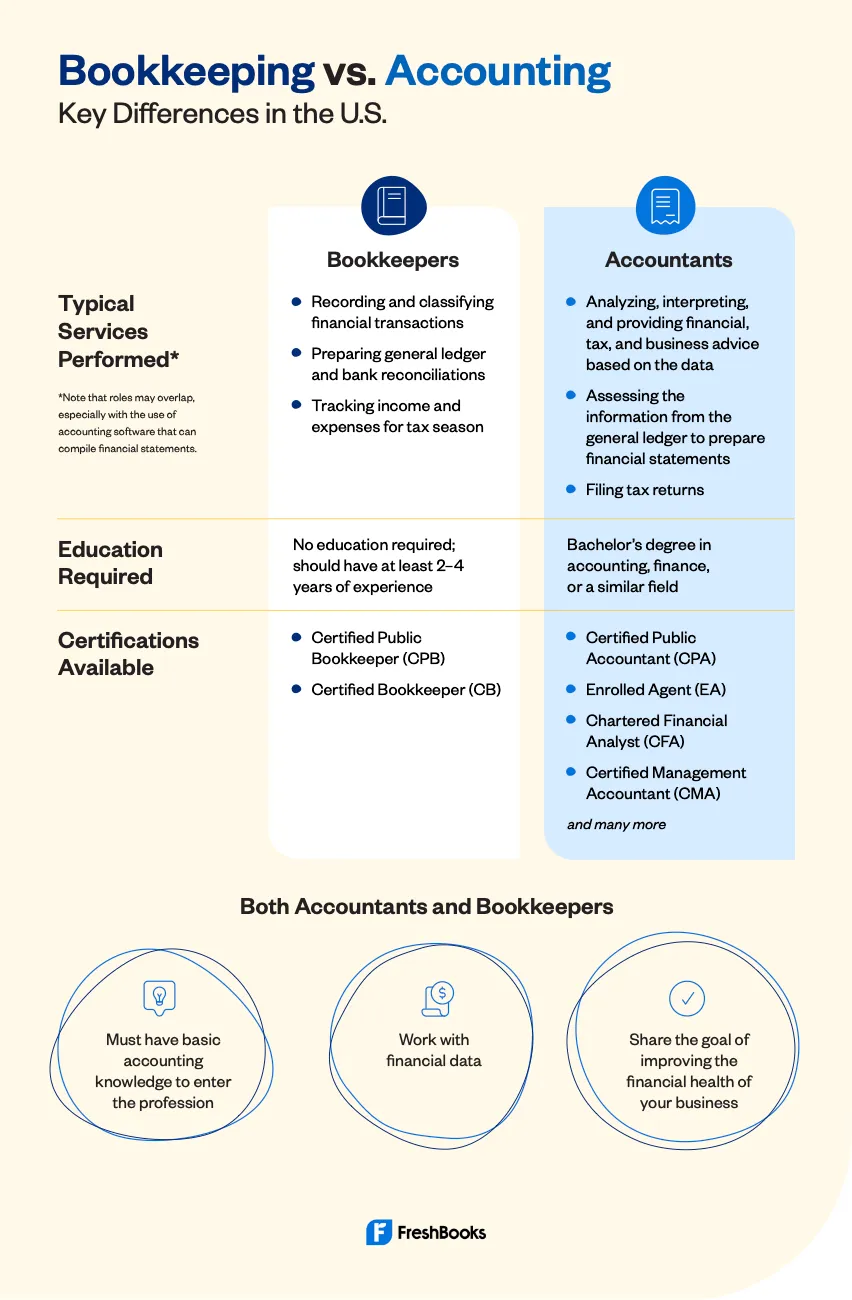

What’s the difference between bookkeeping and accounting? Unless you’re an accountant or bookkeeper, you may struggle to answer this question, and understandably so. On the surface, these professions are very similar: Bookkeepers and accountants both work with financial data and help you manage your finances.

There’s also a blurring of roles, with some accountants providing bookkeeping services and some bookkeepers giving strategic business advice. Plus, today, most bookkeeping software can create financial statements—a task usually reserved for accountants.

Still, accounting and bookkeeping functions are distinct. In this post, we’ll cover the differences and similarities between accountants and bookkeepers and their services so you know which to hire.

Here’s a quick summary of notable differences (and a few similarities) between bookkeeping and accounting.

What Is Bookkeeping?

Bookkeeping is a crucial first step in the accounting process. Think of bookkeepers as athletes who start the track relay. They lay the foundation for accountants by recording financial transactions. Once the first leg of the race is finished, they hand the baton—the financial information contained in ledgers and journals—to accountants to complete the race.

(That’s not to say that accountants can’t and won’t record transactions—they can and often will. This analogy simply illustrates the differences in the traditionally defined roles.)

By recording financial transactions, bookkeepers track your finances so you can view at a glance how much money is entering and leaving your business. And because they’re tax compliant, you can feel confident they’ll keep you on the straight and narrow.

What Does a Bookkeeper Do?

But what exactly are some of the tasks bookkeepers do? Here are 6 common bookkeeping tasks:

- Recording income and expenses. Bookkeepers record financial transactions, including income from products or services and expenses such as rent, utilities, and office supplies.

- Managing payroll. Although payroll is not a core bookkeeping function, some bookkeepers process payroll and assist with payroll tax returns.

- Invoicing and payments. A bookkeeper may create and send invoices to customers and make payments to vendors on your behalf, depending on your arrangement.

- Reconciling accounts. Your bookkeeper will compare the balances in your books against bank and credit card statements to see if they match. If not, they make adjustments and create bank reconciliation statements to record these discrepancies.

- Tracking payables and receivables. Your bookkeeper may track accounts payable (money you owe) and accounts receivable (money owed to you). Bookkeepers keep tabs on all invoices and due dates and follow up with late payers. They will also make sure you pay your bills on time and don’t pay twice. As soon as they make a payment, they record the amount as a business expense in the ledger.

- Maintaining the general ledger. Your general ledger is the master accounting document that stores all your financial transactions. The general ledger typically uses the double-entry accounting method, meaning for every debit on one account, there’s a corresponding credit on another. Your bookkeeper will:

- Post relevant credit and debits to your journal before transferring them over to the general ledger

- Ensure these debits and credits balance

- Record all income and expenses in this way

What Credentials Does a Bookkeeper Have?

Unlike accountants, bookkeepers don’t need specific licenses, certifications, or formal education. Many experienced and knowledgeable bookkeepers honed their skills with on-the-job training.

Some bookkeepers choose to obtain optional credentials through national organizations, such as the National Association of Certified Public Bookkeepers or the American Institute of Professional Bookkeepers.

Other bookkeepers get certified in the bookkeeping software they use with clients. For example, members of the FreshBooks Accounting Partner Program can get the FreshBooks accounting certification, which provides ongoing skills training, tools, and resources to help bookkeepers serve their clients.

These programs are beneficial for new bookkeepers who don’t have much real-world professional experience, but hiring a bookkeeper without one of those credentials can be just as effective for your business.

Do Bookkeepers Do Accounting?

Bookkeepers sometimes do accounting tasks, such as generating financial reports from the accounting software, making journal entries for depreciation and accrued expenses, and more.

However, the conventional function of a bookkeeper is to record daily transactions and keep your books organized. Then they turn that bookkeeping data over to an accountant to provide analysis, advisory services, and prepare tax returns.

What Is Accounting?

An accountant uses the financial data provided by a bookkeeper to interpret, analyze, and report on the financial health of the business. Because they offer more detailed insights that inform business decisions, you don’t want to hire an accountant to only record income and expenses. You’d pay more for the same service a bookkeeper could do for less and, in the process, underutilize the accountant’s expertise.

What Does an Accountant Do?

An accountant can perform dozens of services, but here are 4 core tasks that an accountant performs:

- Preparing financial statements to help you see the bigger picture and assess the financial health of your business, including:

- Balance sheets: A snapshot of your financial situation at a point in time, calculated through this formula: Assets = Equity – Liabilities

- Income statements: A record of all your income and expenses over a period of time

- Cash flow statement: A record of cash flowing in and out of your company for a period of time

- Analyzing journals and ledger entries and making adjustments, e.g., accountants will identify any incurred expenses not yet recorded

- Providing tax preparation services and providing tax advice

- Offering financial advice and helping understand the consequences of your financial decisions

What Credentials Does an Accountant Have?

At a minimum, an accountant must have a bachelor’s degree in accounting. They may also pursue certifications to demonstrate they have the expertise required to serve their clients.

Keep in mind that a designation is not a guarantee. Even if an accountant has a degree and a certification, it doesn’t mean they are a better choice than a bookkeeper with sufficient experience.

While it can be reassuring to see letters after an individual’s name, we recommend focusing instead on finding an accountant who offers the services you need, you feel comfortable with, and trust.

What Is a CPA?

In the U.S., certified public accountants (CPAs) are accountants who have specific training and education and pass a rigorous exam on business and accounting concepts and regulations.

A certified public accountant can perform a handful of accounting tasks that ordinary accountants aren’t allowed to do, such as:

- Issuing audited or reviewed financial statements

- Filing reports with the Securities and Exchange Commission (SEC)

- Representing taxpayers in front of the Internal Revenue Service (IRS; an enrolled agent can also do this)

CPAs may specialize in different practice areas, such as tax, auditing, personal finance planning, or business valuation services. So even though a CPA can file taxes, it doesn’t mean they do.

What Is an EA?

In the U.S., an enrolled agent (EA) is a tax preparer authorized by the IRS to represent taxpayers. To become an EA, they have to pass a 3-part comprehensive exam covering individual and business tax returns or have experience working for the IRS.

So, if you’re being audited or receive a notice from the IRS and need representation, an EA can help.

It’s important to note that some EAs only provide tax services and don’t handle other bookkeeping and accounting work.

Do Accountants Do Bookkeeping?

Some accountants do a bookkeeper’s work by producing financial records from a pile of expense receipts and bank statements, then using that bookkeeping information to advise a business owner on tax planning, business strategy, and more.

However, having an accountant take on the bookkeeper’s role is usually an exception rather than the rule. Most accountants freely admit that bookkeeping is not their strength. They’re more interested in the big picture and don’t have the time or inclination to handle recording daily transactions or organizing financial documents.

Instead, an accounting firm may hire an in-house bookkeeping team or partner with their client’s bookkeeper to provide business owners with the expertise and financial support they need.

5 Signs It’s Time to Hire an Accounting Professional

Accounting and bookkeeping are 2 vastly different professions despite the similarities and blurring of roles. Hopefully, this post helped clarify these differences and similarities to remove any confusion.

Now that you understand how bookkeeping and accounting differ, it’s time to decide which one is right for your business. While this decision is personal and depends on your needs and business goals, here are some signs it’s time to outsource your bookkeeping and accounting needs.

- You’re stretched too thin. Handling your own bookkeeping takes time—a luxury that you as a business owner might not have. If you feel like you’re drowning in paperwork and spending too much time on behind-the-scenes tasks, an accountant or bookkeeper can help.

- You have cash flow problems. Running out of cash is the #1 reason businesses fail. An accountant or bookkeeper can prepare cash flow forecasts and help you devise tactics to deal with cash shortages.

- Payroll is complicated. Once you hire an employee, handling payroll becomes more complex. You might have to withhold child support or retirement plan contributions, calculate payroll taxes in multiple states, and file several payroll tax returns and W-2s. Outsourcing this to an accounting professional frees up your time and helps you avoid penalties for late or incorrect filings and payments.

- You got something wrong. You woefully underestimated a tax bill. You accidentally classified an employee as an independent contractor. You didn’t realize you need to register and pay sales tax in another state. You can’t get a business line of credit because your books are a mess. Accounting and tax weak spots can lead to nasty surprises. An accounting professional can help you get out of hot water or avoid these unwelcome surprises in the first place.

- You hate dealing with accounting. Don’t know the difference between a debit and a credit? Is handling bookkeeper records more likely to put you to sleep than fire up your motivation? There’s no shame in admitting it. Bookkeepers and accountants can take those dreaded tasks off of your plate entirely or help you automate some processes so you can focus on areas where you shine.

Working with an accountant or bookkeeper doesn’t mean losing control of your business. The best bookkeepers and accountants work with you, giving you visibility into your finances and helping you get a better understanding of your company.

This post was updated in May 2022.